Buy in a Buyer’s Market. Sell in a Seller’s Market.

David Steinberg

May 17th, 2026

Share

Facebook

Twitter

LinkedIn

Email

Table Of Contents

First, A Quick Note.

Before I dive in, let me preface this article with something important: I know not every client who’s looking to make a change is able — or wants — to keep their existing property. Sometimes the finances just don’t allow it. Sometimes the goal is to cash out cleanly. Sometimes the math runs the other way and selling outright is genuinely the right move.

But I feel like it’s always worth the conversation. It’s better knowing what your options are than guessing what they might be. All I’m doing here is opening up that conversation — same as I do with every client who phones in. “Did you look at all the options?”“Did you want to explore the option of keeping your house instead of selling it?” Sometimes the answer is no, and we go a different direction. Sometimes the answer changes the whole plan.

Read on.

Buy In A Buyer’s Market. Sell In A Seller’s Market.

There’s a saying in real estate that’s too obvious: buy in a buyer’s market, sell in a seller’s market. Everyone nods. Not everyone actually does it. Because when people want to “move up” or “downsize,” they list their current place first, freak out when it doesn’t sell, drop the price, and end up giving away tens of thousands of dollars in equity. Then they go buy in the same market they just sold into, and feel like they broke even.

I’ll talk about ways that you don’t just break even. I’ll talk about ways to get ahead.

Crowdthink Is A Thing. Avoid It.

I had a great podcast recording with Vincent Baart and Adrian Maclaren last week, and Adrian brought up an interesting point about crowdthink. If what you’re thinking right now is that you’re going to sit on the sidelines and wait for the economic and political picture to clear up before you make a move — read this first.

The crowd right now is sitting on the sidelines. And that’s creating massive opportunity for the people willing to jump in and go against it. Inventory is high. Sellers are motivated. Think about it — once the crowd decides it’s a good time to buy, a lot of people are going to flood the market all at once, and that pressure is exactly what flips this from a buyer’s market back into a seller’s market. We saw it happen just like that in 2019–2020.

So if there’s a lesson to be learned from the past: don’t wait. As Warren Buffett so eloquently puts it — be fearful when others are greedy. Be greedy when others are fearful. It’s a common theme in my newsletters, and couldn’t ring more true in our real estate market.

Look Around. The Inventory Is Stacked.

Greater Victoria had 3,710 active listings at the end of April. That’s up almost 14% from March alone, and 8.3% higher than this time last year. There are sellers out there who are, frankly, getting nervous. Some are dropping price for the second or third time. Some have been sitting for 60, 90, 120 days. You can see it on the listings — the language gets softer, the “motivated seller” stuff starts creeping in.

If you’re a buyer right now? You have leverage you haven’t had in years. Time to look at properties. Time to do your due diligence. Time to negotiate. Time to walk away. That is a buyer’s market.

But Here’s A Problem Facing Upsizers and Downsizers.

If you’re trying to move up — buy a bigger place, get into a better neighbourhood, get the yard — you also have to sell your current home. Into the same market. Where buyers have all the leverage. Where homes are sitting. Where prices are softening.

So what happens? You list your house, you get a soft offer (or no offer), you panic, you accept less than you should, and now you’re trying to win a property in a buyer’s market with weakened buying power. You’re playing offense and defence at the same time.

Here’s What I Do Differently. Risk Management.

I structure the financing so my clients buy in the buyer’s market and don’t have to sell into it, but, almost even more importantly, I run it all through the risk management test.

What could go wrong?

How much would it cost?

How does that affect your life?

What can we do to reduce the risks?

We strategize it out and think about all the items affecting your cashflow. All the risks. It’s what I have to do everyday with each one of my clients. Risk management. It’s not some silly term, it’s the most important one.

Account for all possibilities. What if the real estate market drops? What if rates go up? What if rates come down? What changes personally in your situation, and how does that affect the plan? Can you afford to wait until you sell?

I ask, all the questions. I account for all possibilities.

Because if I’m the one getting you into that extra debt, I better damn well make sure you can afford it.

I’d argue that risk management is the single most important factor in financial dealings – debt AND investing; risk management is at the centre of all of it.

My Bcomm degree wasn’t in marketing, or operations, or international business. It was in Finance, and Risk Management. I was a banker for a long time before I was a broker. And I do risk management, best. Just ask my clients, you can read our reviews.

What I already do for my clients.

By strategizing with me, I enable you to use this buyers market opportunity to get yourself that rental. Because right now, they’re cheaper. Then, when the market shifts back the other way (and it will — it always does), that’s when you sell the first property. Into a seller’s market. For what it’s actually worth.

You bought low. You sold high. Imagine that.

I’m your guy on strategy, my team expertly completes your file.

I’ve probably helped over 300 families upgrade and keep their existing home. The strategy is my thing. Making sure your file gets properly without missing any details, that’s my expert team that makes that happen.

The success of your financing doesn’t just depend on the strategy. It depends on documents and execution. Big details. Little details. We’re detail oriented, and we put that to work for you. Here’s a profile on one of our amazing brokers that helps get your file done. Meet Roxan!

Yes, This Is Actually Doable. Here’s The Mechanics.

The financing is not “off-the-shelf bank-counter” stuff, which is why most people don’t know it’s an option. A few things have to line up:

Down payment for the new place. Usually pulled from existing equity through a refinance or HELOC on the current home — before you buy the new one. Order of operations matters here. A lot.

Qualifying with the rental income. Most lenders will let you use 50–100% of projected rent (depends on lender and property type) to offset the mortgage on the place you’re keeping. Some are way more friendly to this than others. That’s where I add value — knowing exactly which lender to send this to.

The right product on the new mortgage. Some products penalize you for carrying a second property. Others reward it. Choosing wrong here costs you real money over five years.

Cash flow stress test. I run the actual numbers — what the rental brings in, what it costs to carry, what your new payment looks like, where you sit month-to-month. If the numbers don’t work, I’ll tell you. I’m not in the business of stretching clients thin.

This is the kind of structuring that takes a 30-minute conversation, not a click-a-button bank app. It’s exactly what I do all day.

Downsizers — This Applies To You Too.

Same logic, flipped. If you’re trying to downsize and your big house won’t sell, you’re stuck. But if we can finance the smaller place using equity from the bigger one — without selling first — you move on your timeline, not the market’s. Then you sell the family home when the market comes back. Maybe you rent it for a year or two in between. Maybe a kid lives in it. Maybe it sits empty for a few months and that’s fine, because the math still works.

The principle is the same: don’t let a soft seller’s market force you to sell at a discount.

When Does The Market Shift Back?

Honest answer: I don’t know. Nobody does.

What I do know is that real estate works in cycles. So while we may not have the timing on when we move back to a sellers market, we know it eventually will. Vancouver Island is not getting any less popular. The people who bought at the bottom of every previous cycle in this city look like geniuses now. They weren’t geniuses. They just bought when other people were scared.

This is one of those windows.

Real Estate is a Long Term Hold (or at least until the sellers market).

This strategy isn’t for people expecting to keep the 2nd property for a year, and then sell. You should be prepared to keep your property for 5 years. Why? Generally, somewhere within every 5 year period we have a sellers market.

So while we may not see that sellers market for 1 year or 2 years, you can probably expect we’ll see it in 3 or 4 years.

This plan is all about setting up your expectations correctly. Think long-term.

Find Good Renters. I Have Tips.

I always speak to folks who are scared of being landlords, and rightly so. Why? We always hear the stories about nightmare renters, and rarely hear stories about great renters. Here are some great tips on finding awesome renters.

Price your rental just below the market rate. Why? If you price your rental aggressively, you’ll sweep in way more qualified applicants. You’ll have your choice between lots of good potential tenants. Who cares if you give up $100 or $200 a month!? The small amount of money you may give up will more than make up for itself when you have strong, long term tenants.

Allow pets, as long as the situation allows. I see rental listings saying “no pets”. Guess what those landlords are doing? They are discounting all the good and responsible tenants who have a dog or a cat. Think about it. Many pet owners are in fact MORE responsible than people who may not have a pet. They want their pet to have a long term home. They don’t want to move a lot. They are professionals who have the extra cash to care for their pet. Do you really think a responsible pet owner is going to allow the pet to ruin your place? I always say, who cares if the dog scratched the floor a little bit? I could care less about scratches on the floor and the walls if the tenants are good and stay for a long time. Oh, and you can charge a pet deposit too, along with your security deposit.

Do your homework. Don’t just trust anyone’s word. Get references. Collect paystubs. Ask for a credit check. Don’t say yes right away. Trust your gut, too.

Always meet your renters in person. Be weary of anyone who says they are representing someone else because they are out of town, or whatever the reason may be. Even if it’s not a scam, there is less of a chance of things going wrong if the people you show the home too are going to be the ones renting it. Don’t just be ok with family viewing a house for out of town people. More things can go wrong when the out of towners move in.

Document everything. The BC Tenancy agreement is a good document to use. Fill it out completely. Lay everything out on paper. Don’t leave anything up for guessing.

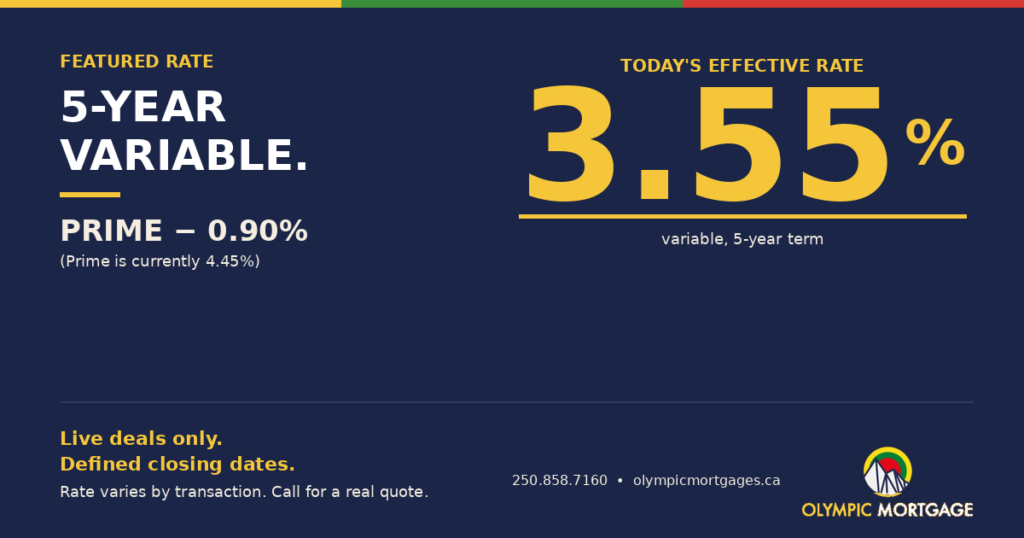

A Quick Note On Rates — We’ve Got A Good One.

Right now we’re sitting on a Prime minus 0.90% variable — that’s 3.55% today. That’s a sharp rate. It’s the kind of pricing that, a couple years ago, would’ve had people lining up. It’s actually getting pretty close to the rate special I wrote about, now 2 years ago. When we have P-1.00% for everyone.

Today, this rate special is barely making headlines because the market has been so focused on what might happen next.

And yes — there’s chatter about rates going up. The oil shock out of the Middle East has pushed inflation expectations higher, and markets are starting to price in the possibility of a hike or two later this year. But here’s the other side of that picture: the Canadian economy is still soft. Unemployment is sitting between 6.5% and 7%. Business investment is weak. Growth is uneven. That’s not the economic backdrop where the Bank of Canada hikes aggressively.

My read — and reasonable people can disagree here — is that a lot of the inflationary fear is being driven by temporary shocks (energy prices, geopolitical noise), not the kind of sustained domestic demand pressure that forces the BoC’s hand. Variable, in this environment, is a strategic play. Not for everyone — but for the right client, absolutely.

Important Caveat: Rates Are Transactional.

One thing I always tell clients up front — a rate quote in a newsletter is not a rate quote on your deal. Mortgage rates are highly transaction-dependent. Is it a high-ratio insured deal or a conventional one? Is the mortgage $300,000 or $1.2 million? Is it a purchase, a refi, or a switch? Is the property owner-occupied or a rental? Every one of those factors moves the number. Special pricing like Prime minus 0.90% is held only for live deals with a defined closing date — it’s not a parked rate you can shop around with for six months. If you want to know what you’d actually qualify for, the only way to find out is to run the numbers. That’s a 15-minute conversation.

A New Bank Just Joined The Roster.

We’ve always had great partners in the BIG RED and the BIG GREEN, and I’m happy to say we’ve now added the BIG BLUE (BMO) to our roster of bank lenders. Why does that matter to you? More options, more competition for your business, and — most importantly — another bank in our corner for the deals the other two won’t touch.

Every bank has its quirks. Every bank has files it loves and files it won’t look at. Adding the BIG BLUE means one more tool in the toolbox when a client’s situation doesn’t fit cleanly into the first two boxes. That’s exactly what we do well at Olympic — getting the out-of-the-box clients approved with better rates and better terms than they’d get on their own. With three big banks now in our arsenal, we’re sharper than ever at it.

So Call Me. Seriously.

If you’ve been thinking about upgrading, downsizing, or buying an investment property and you’re stuck because “we have to sell first” — we probably don’t. Let’s spend 15 to 30 minutes on the phone. I’ll look at your numbers, your equity, your income, your goals, and tell you straight up whether this strategy fits.

If it doesn’t, no harm done. If it does, you might be looking at the smartest financial move you make this decade.

250.858.7160. Even on weekends.

Signing off for now,

David Steinberg Owner & Lead Broker — Purchasing Strategist Olympic Mortgage david@olympicmortgages.ca | 250-858-7160 | olympicmortgages.ca

Mortgage Rates and Economic Update Mortgage rates have eased over the past few weeks. With the conflict in the Middle East settling down, energy prices have started to come back to earth — and the expectation is that inflation cools along with them. Bond yields have softened in response, and fixed mortgage rates have followed […]

Thank g-d I didn’t have any money invested in Bitcoin, myself. Yeesh. That stuff is way too risky. It’s a long one today. In summation, I’m going to talk about the tech bubble/stock bubble, what Tiff Macklem is actually saying to us, what’s going to happen when the bubble bursts, and finally, the kicker, what […]

At Olympic Mortage, we want the best for the people around us. We care for our clients, whomever they are, wherever they’re from. Everyone gets the best of us, because that’s what we want to be putting out to the world. So go ahead, try us.

CONTACT DETAILS

Suite 103, 2311 Watkiss Way, Victoria, BC, V9B 6J6