chat gpt. You see, I’ve always written my own articles, but I merely asked chat GPT for the image, and then it just threw out the article along with the picture.

As I was in a rush, I started reading what chat gpt had given me, and it was “OK”, at best. It generated alot of lines that sounded “digital markety” to me, rather than what I might feel is real writing.

Anyways, I went through it, took away what I really hated, added some of my own, and here we are. I’ll keep this updated and with extra commentary as the mortgage landscape changes.

If you’ve ever wondered where you actually fit in the mortgage world—you’re not alone.

Most people think mortgages are black and white:

In reality, it’s not that simple. There’s a spectrum of the types of mortgages available to you.

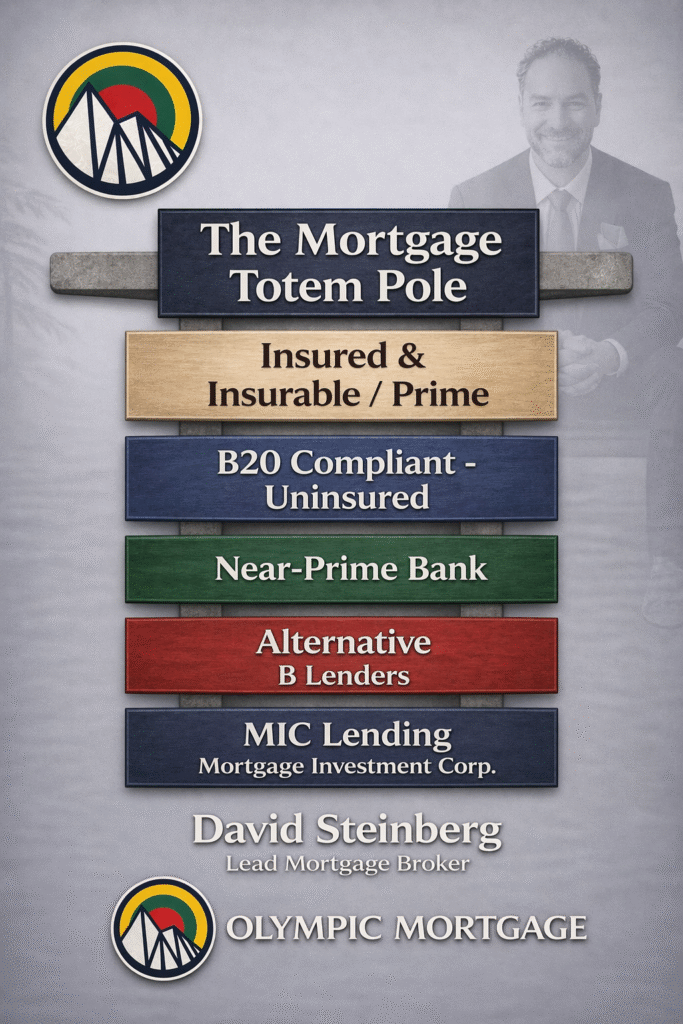

Think of it more like a totem pole.

And understanding where you sit on that totem pole can make the difference between:

So before you stress about rates or approvals—let’s break this down properly.

There are five main levels of mortgage lending in Canada. Each tier is unique in the qualifications required for that type of mortgage, interest rates offered, and even if there is a fee, or no fee.

Each tier serves a purpose and each one has a place.

This is where everyone thinks they are—and where most lenders compete on rate alone.

This tier is considered the insured and insurable mortgage tier. Meaning, everyone has to qualify on a very strict set of guidelines set out by the three main default insurers in Canada – CMHC, Sagen (formerly Genworth formerly GE), and Canada Guaranty. There are no exceptions to the guidelines, no outside of the box lending.

Also, for this tier, only purchase transactions and straight switch transactions qualify. If you already own a house and want to borrow more money out of it, that would be considered a refinance transaction, and that falls under the tiers below.

Typical borrower profile:

If this is you, things are simple:

The rates offered by lenders here are the lowest you’ll see in the industry. If you qualify, then you can trust the rate is going to be very competitive.

What is B20 compliant? OSFI, the banking regulator in Canada, has set out general guidelines for banks to abide by when underwriting mortgages that are not insured or insurable (the top tier). These are the B20 guidelines.

Click the link for a very good video, straight from our friends at OSFI, explaining the B20 guidelines.

https://www.osfi-bsif.gc.ca/en/about-osfi/multimedia-library/guideline-b-20-explained

This tier is for all of those who don’t qualify on insured or insurable guidelines, but still qualify within a set of guidelines for debt servicing and credit. For example – in the top tier, the maximum debt servicing ratios have to be 39%/44% GDS/TDS, whereas in this tier, as long as the TDS is within 44%, it will still qualify under the B20 guidelines.

In the top tier above, no refinance transactions are allowed. No equity take-outs, and no home equity line of credits. In this tier, as long as the borrower qualifies under the guidelines, they can refinance their home to pull money out for their usage.

This is your tier of regular bank mortgages.

This is where things get interesting—and where many real-world borrowers fall. You see, the banks have a very small part of their lending portfolio that is considered “non-compliant”, meaning, it does not qualify under the B20 guidelines.

The banks don’t really advertise this level of mortgages, because the basket of funds they are pulling from, the non-compliant basket, is a much smaller basket than the insured and insurable basket or the B20 compliant basket. While the banks are very willing to lend in the top two tiers, the banks get very choosy when considering borrowers for their non-compliant mortgages.

Basically, if you have good credit and a high net worth, but the mortgage just doesn’t qualify under the top two tiers, you’ll be considered for this basket of lending.

You might be here if:

This is the part of the totem pole that doesn’t get talked about enough. Most brokers may default harder to put together deals into the alternative lending realm (below), rather than figuring out how to make the borrower fit into this near prime box.

Most deals in this range don’t get declined—they get misunderstood.

Banks are built for clean, simple files. But real life isn’t always clean or simple.

And this is where:

This is also where we as mortgage brokers shine. Since 2009, David and team have been helping tons of Canadians fit into this tier. By strategizing the mortgage properly, by telling the right story, and by working with lenders and banks that can stretch the limits on their near-b files.

Further down the totem pole, you’ll find alternative (B) lenders. Here, borrowers just don’t fit in the top three levels, but still need to qualify for a mortgage.

Here, borrowers need a minimum of 20% down, and most lenders will charge a fee to do the lending. These lenders are still scheduled banks, but on the fringe. Lenders that we use often are Haventree Bank, National Bank, Equitable Bank, and Bridgewater Bank. Also, many of the monoline lenders that lend in the top two tiers have also created departments within their companies to do B and alternative lending. Here, we have First National Excalibur, CMLS Aveo, and RMG Eclipse, just to name a few.

This level is for borrowers who:

These mortgages typically come with:

But here’s the important part: This is not a failure—it’s a strategy.

Used properly, alternative lending is:

At the bottom of the totem pole is Mortgage Investment Corp lending.

In short, a mortgage investment corp, or MIC, is an investment pool where investors pool their funds, and then the MIC lends out those funds to those who don’t qualify (or don’t want the document hassle) of the upper tiers.

MICs are very flexible on their guidelines, and almost never worry about debt servicing. MICs are focused on the equity in the property. If you have a higher amount of equity in your property or a higher downpayment, and only need to borrow, let’s say, up to 65% of the value of your home or the purchase, you’ll qualify for the MIC mortgage. Sometimes, MICs will lend up to 75% or even 80% of a property value, but only for very strong deals and only if the deal makes sense.

The MICs are looking at the real story. They want to see that their borrowers have a properly planned out exit strategy, so that when the mortgage comes due in 1 or 2 years, the client will be able to pay off the mortgage or move the mortgage up the totem pole.

This is typically used when:

MIC lending is:

MICs price their deals when they underwrite them, meaning, there are really no set rates that we can quote our clients. The stronger the deal with higher equity, the lower the rate. MICs can lend as low as 5.25%, but we rarely see anyone get these rates. The rates are more around 7% to 9% or thereabouts, and usually the MIC will charge a 2% fee, and pay 1% to the broker involved.

Sometimes, in deals that make sense, our brokerage can lower our fee to get a non-complicated deal finished with less cost.

MIC mortgages make sense for those who need to borrow but don’t have another option.

Here’s the part most people miss:

Where you sit on the totem pole isn’t really the problem.

The real issue is how your deal is structured.

We’ve seen it many times:

If your income isn’t simple, your mortgage strategy shouldn’t be either.

If you’re not sure where you fall on the totem pole—that’s normal. Most people aren’t.

But if any of this sounds like you:

Then you’re exactly the type of client that benefits from the right approach.

Not a different mortgage. Not a riskier lender. Just the right structure.

Signing off for now,

David Steinberg, AMP, BComm

Lead Broker and Owner at Olympic Mortgage