Just like I try to simplify my client’s lives by being instrumental in their purchase, debt consolidation, or whatever-it-is, I realize that I too have to simplify some aspects of my business and life that have become a little too confusing, or cumbersome, to me.

A bit of a reset, so to say.

Among other things, I’m simplifying my marketing. If anyone wants to find the best rate, they have to find it here, on the website, in whatever latest blog post I’m doing.

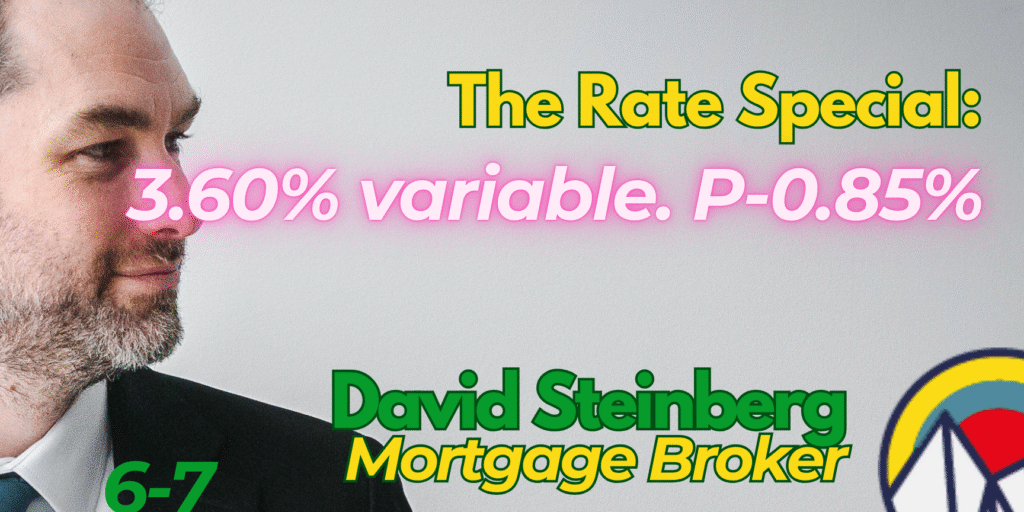

Before we talk about rates, 6-7.

I had to. I have two teenage boys and I myself am a bit of a kid, so yes, 6-7 became a thing with us. It’s immature and stupid, but hey, in some ways I still have to live like a kid, just to keep that young person in me, too. Sorry, not sorry.

First, let’s be honest about this game of interest rates.

Every bank and broker’s disclosure on their best rate is that the rate is subject to change at anytime, until you have something concrete, on paper. And no, emails don’t count. Same goes for verbals too. You just can’t depend on them.

Until you get a bonafide commitment, any bank or broker could blow any amount of smoke up your ass with regards to what interest rate you can get. *scuze my language, but it’s been frustrating to see how much smoke there is!*

The verbal rate you received doesn’t amount to anything.

I have the ability with my low rate lender to beat other’s rates, but I’ll only consider playing that game when I see something on paper. And terms have to be the same too, bucko. Let’s compare apples to apples.

In this business, anyone can tell you anything, and then renege at the last minute. The classic bait and switch. And no, there’s no recourse for you. You can’t complain yourself into a better rate. You’re stuck with what they can get you, even though it wasn’t the same as what they told you at the start.

Because mortgage rate shopping has become way out of hand.

First of all, I get it. This is your biggest expense out of all of them. Everyone has to save money on their mortgage, and I don’t begrudge you for wanting to play the “mortgage shopping game”.

I don’t really like games, and I don’t want to play into the whole mortgage rate shopping game. So don’t blame me for simply changing the game altogether. When you look at my best rate, please read the “how to get this best rate” steps that come afterward.

To those that trust us from the start, and to existing clients:

You guys are awesome. My existing clients know that I’m going to bat for them to get the best rate, and they don’t incessantly shop. They understand that it’s my job as their broker to get them the best rate.

My clients win, every time. You can see that from our amazing google reviews, and we have the most of those google reviews in Victoria.

My existing clients are all amazing, and get the program. They know I’ll go to bat for them, every time.

Let’s start with that 15 minute call.

Let’s get this straight though. I give everyone their 15 (to 30) minutes. During that call, I can determine where you are on the lending totem pole, and which rate you’ll be eligible for. I’ll let you know during that conversation.

It’s up to you after that initial conversation whether to take things to the next step with us, or whether to keep shopping around.

You can only take advantage of the best rate, when…..

…..we have some commitment from you.

This means that you’ve done all your other mortgage shopping. If you feel the need, fill your boots. Go to every bank and broker and ask them their best rates, put applications in, whatever. I double dare you. But I won’t put pen to paper, or even start working on your application, until you’ve confirmed with us that you’ve finished your mortgage shopping elsewhere. We’re your last stop. Easy. Simplified.

I give actually true second opinions.

I love giving second opinions, actually. True ones. You can see in our reviews that there are some that have called me to ask me if I can do better than what they’ve got. I’m always honest. I’m not here to waste my time, or yours.

If you have a great rate from your existing bank or broker, I’ll tell you to stick with it. If the rate they gave you is only OK, I’ll tell you if I can do wayyyyyy better.

Then you decide after that 15 minutes if you want to take the next step.

And finally, here it is:

But before you get all excited that the rate is yours, please read on and I’ll let you know the ins and outs of getting this great rate.

Details behind getting the best rate:

We’re going above and beyond with our lender to get this rate for our clients. So we know we can only send them super serious clients. They don’t want their time wasted, and we don’t either.

Here are some basics for understanding if you can score this super low rate:

You have to be ready to go, and you’ve done all the mortgage shopping you need to.

It doesn’t matter if it’s been approved elsewhere. We can get you reapproved for this rate, and it doesn’t put you “at risk” of losing your last approval (unless I tell you otherwise).

We need a full document file before we submit to this lender, along with your consent to pull your credit bureau.

File has to be pre-qualified by our high standards. This isn’t the type of rate where we can get a ton of exceptions on things like income, credit score, or generally any creativity on your file. If you need creativity, I’m also the best at that, (give me a call 2508587160).

This rate is specifically for high ratio insured files of a minimum size. Call for your specific rate quote.

#1 – You gotta be ready to go, and you’ve done all the shopping you need to.

Doesn’t matter if it’s been approved elsewhere. We can get you reapproved for this rate, as long as you’re high ratio and insured. It doesn’t put you “at risk” of losing your last approval.

When we say you have to be ready to go, we’re saying you need to have your documents in order, a live deal on the table, and already done all your other mortgage shopping (because when you secure this rate you won’t need to do any more shopping).

The lenders really giving us a break here by giving us this crazy low rate, so we’re making sure that we’re only sending them serious borrowers.

#3 – Full document file, well qualified file (and if you’re not, call me anyways and I’ll sort you out)

Don’t worry though. When you start working with us, we will help you put the file together. That’s part of our job in being great mortgage brokers. We help you get the documents, we walk you through the process. We help you along the way.

If you’re not well qualified, call me anyways. I’m the expert on getting things that are on the edge, through the AAA lenders. Whether it’s an easy approval, or a hard one, we at Olympic Mortgage are your best bet.

#5 – This ones for high ratio, less than 20% down, minimum file size.

If you have 20% or more down, I’m really sorry, but this isn’t your rate. You see, the lenders give the best rates to those that have less than 20% down, because in that scenario, the client is paying for the high ratio default insurance premium.

Mortgage Rates and Economic Update Mortgage rates have eased over the past few weeks. With the conflict in the Middle East settling down, energy prices have started to come back to earth — and the expectation is that inflation cools along with them. Bond yields have softened in response, and fixed mortgage rates have followed […]

Greater Victoria has 3,710 active listings and sellers are getting nervous. That’s a great time to buy — but a terrible time to sell. So how do you upgrade or downsize without giving away equity? Keep your existing property as a rental and time the sale for the next seller’s market.

Thank g-d I didn’t have any money invested in Bitcoin, myself. Yeesh. That stuff is way too risky. It’s a long one today. In summation, I’m going to talk about the tech bubble/stock bubble, what Tiff Macklem is actually saying to us, what’s going to happen when the bubble bursts, and finally, the kicker, what […]

No matter where you are in the buying process, its always the right time to setup a call with a mortgage specialist!

At Olympic Mortage, we want the best for the people around us. We care for our clients, whomever they are, wherever they’re from. Everyone gets the best of us, because that’s what we want to be putting out to the world. So go ahead, try us.

CONTACT DETAILS

Suite 103, 2311 Watkiss Way, Victoria, BC, V9B 6J6